Financial Fundamentals: The Four Basic Financial Statements and What They Say

For a business, financial accounting data is traditionally communicated to internal and external stakeholders through standard reports called Financial Statements. These statements act as the “report card” of the business, allowing a reader to quickly understand what the business has reported on its books, and what it has been doing during the reporting period (usually one year). Having a clean set of financial statements is critical to understanding the true financial position of a company, and essential if that company wants to secure a loan.

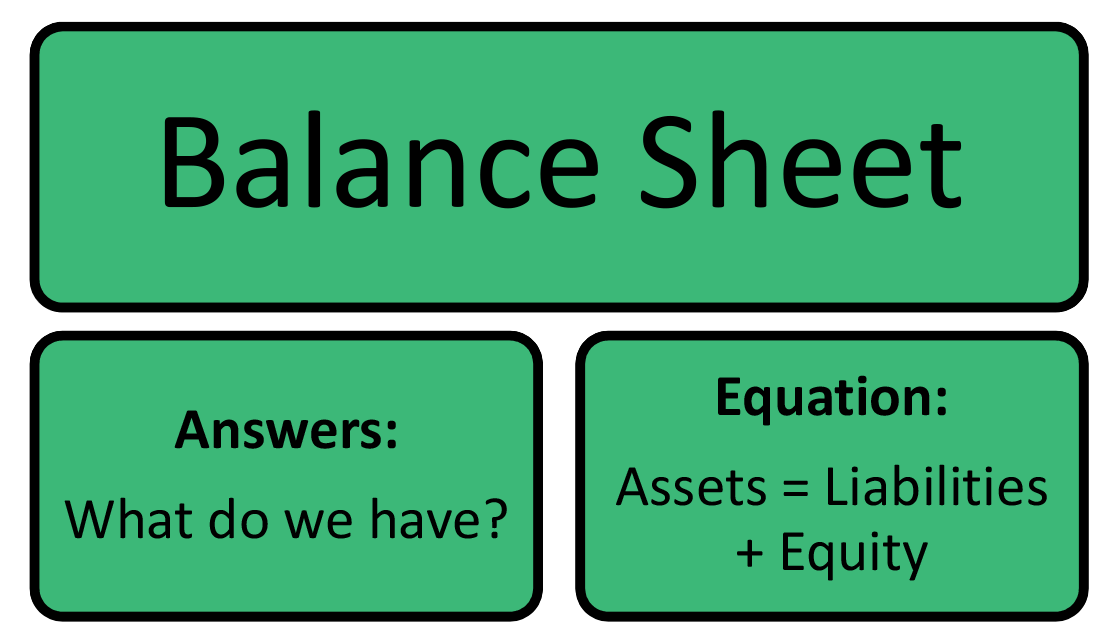

The balance sheet considers a businesses’ financial position at a point in time. This statement can be divided into 3 major sections:

Assets - What the business owns (Cash, Equipment, Inventory, Prepaid Expenses, Receivables)

Liabilities - What the business owes (Payables, Loans, Customer Deposits)

Equity - Money (or deficit) attributable to the business owners (Retained Earnings, Stock, Additional paid-in capital)

The asset section of the balance sheet can be further broken down into current assets (convertible to cash in one year or less) and non-current assets. Similarly, the liability section of the statement can also be broken down into current liabilities (due within one year or less) and non-current liabilities. Every business will have a different definition of what a “healthy” balance sheet looks like, but in general, having a positive current ratio and positive equity balances is a good place to start.

The income statement considers a businesses’ activities over a period of time. This statement is the driver behind the famous term “bottom line”, which refers to the bottom line of the income statement: Net income. The income statement can be broken out into two major sections:

Revenues - Amounts generated from the sale of goods and/or services

Expenses - Amounts spent on business activities during the period (Salaries, Cost of Goods Sold, Loan Interest)

Businesses with multiple revenue streams may choose to break out revenues into different categories such as service revenue and product sales revenue. Some organizations also show expenses broken out into different categories on the face of the income statement to provide more context to the reader of the financial statement.

The statement of cash flows answers one of the more common questions people have when starting a business: “Where did the cash go?” Most companies that produce a set of financial statements will report on the accrual basis of accounting, which means the income statement will not necessarily answer this key question. A traditional statement of cash flows is broken up into three sections:

Cash flows from operating activities - Shows cash inflows and outflows related to current assets and current liabilities such as accounts payable and accounts receivable

Cash flows from investing activities - Shows cash inflows and outflows related to non-current assets such as equipment

Cash flows from financing activities - Shows cash inflows and outflows related to non-current liabilities and equity such as loan payments and contributed capital

The final and least used basic financial statement for small businesses is the statement of equity. This statement summarizes the changes in equity over the reporting period (usually one year). Common lines on the statement of equity for a smaller business include:

Contributions - Money contributed to the business by an owner

Draws / Distributions - Money taken out of the by an owner

Net Income - At the end of the reporting period, the net income (or loss) is brought into equity so a new reporting period can begin

This statement is typically used only by third parties in evaluating the condition of the business when determining whether or not to provide financing to the business and is not usually used by management in the ordinary course of business.

For those who are new to accounting concepts or are starting their own business, knowing these statements is essential to understanding how a business is doing financially, especially the income statement and the balance sheet. Businesses with a growth mindset tend to be very income statement oriented and focus on increasing revenues and decreasing expenses to help expand the operation. While growth is certainly important, it is crucial that a business not neglect its balance sheet, as it can indicate how much resources may be available to fund the next step in growth.

Thanks for reading Financial Statement Fundamentals! If you are interested in going more in depth on financial statements, we highly recommend investopedia and accountingcoach. If you have any questions about your personal financial statements or financial statements for your business, please feel free to contact us!